AI buzz provides a big wake-up call

RELX

Market cap £64 billion

9-month revenue growth 7%

It takes a lot to jolt the sleeping giant that is Relx. The data specialist has quietly ascended to become one of London’s ten most valuable companies, with a market cap of more than £60 billion.

However, questions over whether the rise of generative artificial intelligence threatens to upend the group’s core business, selling information and analytics to professionals in the legal, insurance and medical industries, among others, have sparked a rare sell-off in the shares.

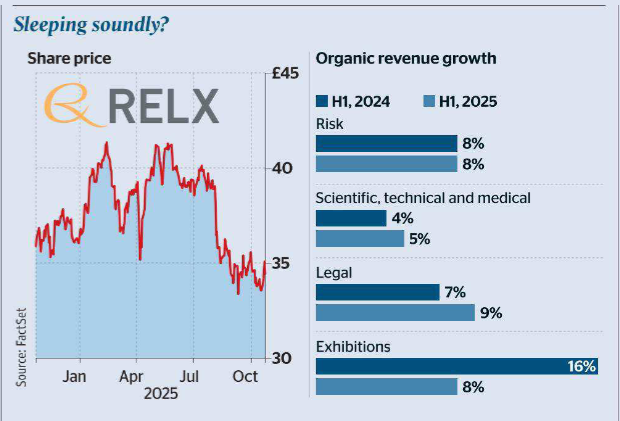

The shares have fallen about 15 per cent over the past six months, although that doesn’t make them cheap by conventional standards, still trading at roughly 25 times forward earnings, but that multiple is down from about 30 in April.

Yet Relx’s premium status is deserved. It has established a long record of stable revenue, margin improvement and sturdy cash generation. Charging customers a subscription fee for the use of its hefty legal, medical and scientific journals means a chunk of its revenue is recurring. Despite the recent headwind, the shares have risen 197 per cent over the past decade, easily outpacing the 51 per cent return generated by the FTSE 100.

The company makes relatively few headlines, and Erik Engstrom, the Swede who has led the business for the past 15 years, has never given a media interview as its chief executive.

Known as Reed Elsevier from 1992 until 2015, it was once a producer of books and magazines but has made a gradual transition away from physical media, selling one of its last print magazines in 2019. It now generates 83 per cent of its revenue through digital means, with face-to-face exhibitions accounting for 14 per cent and print just 4 per cent. Relx now has four divisions: scientific, technical and medical (otherwise known as “STM”); risk; legal; and exhibitions.

In the debate over whether the emergence of ChatGPT and other chatbots will make Relx’s information and analytics tools redundant, the group seems to be winning.

The risk division, which covers the company’s analytics and decision tools for areas such as digital fraud and identity checks that are mission critical for the banks and insurance companies that use them, has long used so-called extractive AI. Those products use machine learning to extract and analyse key bits of information, and were credited for helping kick the business’s underlying revenue growth, which stood at 8 per cent over the first nine months of the year.

However, it has extended its use of AI to its legal and STM businesses, which has driven an improvement in top line performance for both divisions. While its revenue growth has not shot the lights out, adding value through generative AI has pushed it to a rate of 9 per cent, from 2 per cent in 2019. Likewise, STM has improved to 5 per cent from 1 per cent over the same timeframe.

Within the mix, exhibitions may look out of place, not least because it carries more risk that a macroeconomic slump could hit revenues. However, there are no plans to sell it.

Covid hit aside, the business, whose trade shows range from Comic Con to the London Book Fair across 25 countries, has generated respectable top line growth. Over the first nine months of the year, underlying revenue rose 8 per cent, but over the last decade it has fluctuated to a greater extent than Relx’s other three arms.

One of the core tenets of Engstrom’s strategy is to keep a tight enough handle on operating costs that revenue growth outpaces it each year. The result has been consistent margin expansion, which stood at almost 35 per cent over the first six months of the year, compared with just under 32 per cent in 2019.

Its fiscal discipline extends to the way it uses its cash. It has eschewed large-scale M&A in favour of bolt-on deals that may give an edge to its products. Instead most of its cash is invested back into developing its existing technology, and then funding the dividend and potentially share buybacks.

Relx’s record of steady compound returns seems like it can withstand the AI noise.

ADVICE Buy

WHY Share price weakness is an opportunity

No comments:

Post a Comment